Taking Advantage of a Real Estate Market Gone Mad

The so-called BRRRR strategy (Buy, Rehab, Rent, Refinance, Repeat) has been very good to me and, all things being equal, amounts to the best way to invest in real estate in my opinion.

The only problem is that all things are not equal right now. Indeed, the market is insane at the current moment. In Jackson County, MO, where our office is located, there is only 0.8 months of inventory left on the market. A “balanced market” that favors neither sellers nor buyers is six months.

Across the entire country we are seeing this madness. According to Forbes,

“Home prices hit an all-time high of $359,975 in the four-week period ending November 21… This was up 14% year over year, the largest increase since early September… Active listings fell 22% from 2020 and 41% from 2019.”

Almost half (43 percent) of listed homes sold above the list price. For one cozy five-bed, five-bath, 5000-sq. ft. home in Chevy Chase Village just outside of Washington D.C., it sold for a cool million dollars over the list price!

The BRRRR strategy involves buying properties and being all in for no more than 75 percent of their ARV (After Repair Value) and then proceeding to the last three R’s; rehab, rent and finally refinance out your original investment so you have no (or little) money left in the deal.

Unfortunately, in this market, there just aren’t an abundance of deals sitting around that you can “BRRRR out” on. Yes, they still exist. But they are quite rare. After all, who would get foreclosed on in a market that is increasing “14% year over year.” If you fall behind on your payments, just list your house and you have a better than 50 percent chance of getting the property under contract in the first month and a 43 percent chance to getting an offer over the asking price.

The same would go for a tired, out-of-state landlord or new inheritors of an unwanted property or whatever. The market is so hot that it’s hard to be a particularly motivated seller. It’s just too easy to sell.

Likewise, it’s hard to find “value add” opportunities because, well, every other investor is looking for the same. There’s just too many investors chasing too few deals for anything other than the rare gem that slipped between the cracks.

So What Should Investors Do?

Well I’m glad I asked on your behalf.

To elucidate my recommendation, I would start on a brief trip down memory lane. I have a lot of nostalgia for back in 2011 when we first got to Kansas City. We would focus on buying bank owned houses and small multifamily properties and good Lord… they were everywhere. We would go on “property tours” and look at some 15 REOs, make offers on 12 or 13 of them and get one or two under contract.

And oh the prices… don’t even get me started!

There was just a never-ending cornucopia of cheap real estate to buy. But, you might ask, why did we settle for only buying one or two of those 15? Well, obviously the problem was that we couldn’t afford to buy more. (Rehab and property management infrastructure concerns also played a role.)

The major reason we couldn’t afford to buy more is because banks simply weren’t lending. Between 2011 and late 2015 we found exactly one bank that would lend to us. And it wasn’t for a lack of trying to find more.

Anyways, the terms they gave us were as follows:

6.5 Interest

15-Year Amortization

2-Year Seasoning (We had to own the property for two full years before they would lend on the appraised value and not just the cash we had into it.)

In other words, the lending environment back then was trash.

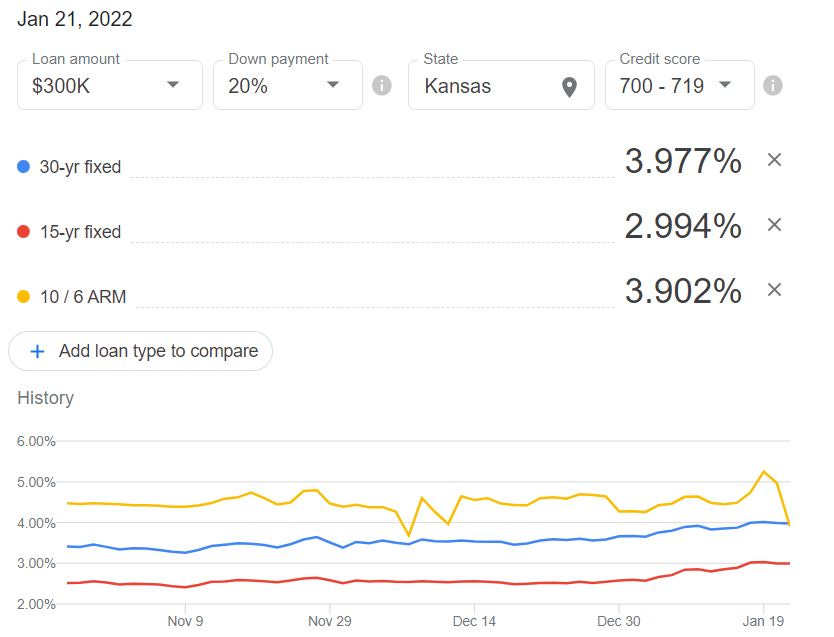

Nowadays, I just got a 3 percent interest loan on my home. And our investment loans are usually just over 4 and no higher than 4.5 percent. And that’s from a multitude of banks that are all eager to lend to us. Back in the nostalgia-inducing, good ole days, we had to rely almost exclusively on private lenders.

So the moral of the story is that back from 2011 to 2015, there were tons of great deals but financing was terrible. Between 2016 and about 2019 there were still good deals, albeit less, and the financing was OK. Now there are very few good deals but the financing is incredible.

I mean, look at this:

Every market has its good points and its bad.

In this market, at the same time as you can get a sub-3 percent homeowner mortgage and 4 percent(ish) investment mortgage, the inflation rate is a full 7 percent with no signs of slowing in the near future.

Effectively, this means that with a 4 percent interest mortgage, you are making money just by borrowing it (assuming you can break even on the cash flow, of course). A 4 percent mortgage is making (in real terms) 3 percent a year over inflation. (Assuming inflation stays high as it likely will for reasons discussed below.)

You should never buy at market prices if you can help it. But demanding a full 75 percent ARV BRRRR deal in this market means you’ll likely just be sitting on the sidelines waiting. And that’s not a good idea when your savings will be depreciating in value every month!

If you have any higher interest debt, now would be the time to refinance. Although make sure you go with a fixed rate mortgage for as long a fixed period as the bank will give you. I don’t see there being any chance rates will go down so avoid adjustable rate mortgages for the foreseeable future.

House hacking or buying with an FHA loan (96.5 percent LTV) are both good ideas now. As is finding a partner or private lender to help with the down payment. Basically getting into real estate with long term, fixed-debt right now is the best strategy. It’s the new BRRRR.

Whatever you need to do that, within reason of course, is what you should pursue.

But What if the Market Crashes?

One of the best parts about the BRRRR Strategy is that it provides an equity cushion if the market crashes. If you are all in for 75 percent of a property’s value and the market goes down 10 percent. Well, it’s not that big of a deal as you still have that 15 percent equity to protect your initial investment.

That won’t be there if you put BRRRR to the side as I am recommending. I would still highly advise getting at least a bit of a deal; 10 percent equity would be good to aim for. That is still attainable in this market and gives you a bit of a cushion.

That being said, while I have no crystal ball, I don’t see the market crashing. Yes, the Dow Jones has tumbled a bit of late and we are due for a recession sooner or later. But not like the last one. For one, unlike in the run up to 2008, there are not a flood of stated income prequalifications, teaser rates and the infamous, NINJA Loans around these days.

Secondly, before 2008 the United States did not have a housing crisis. Today it most certainly does. As a Freddie Mac analysis notes,

“As of the fourth quarter of 2020, the U.S. had a housing supply deficit of 3.8 million units. These 3.8 million units are needed to not only meet the demand from the growing number of households but also to maintain a target vacancy rate of 13%. Between 2018 and 2020, the housing stock deficit increased by approximately 52%.”

Between 2000 and 2007, there were at least 1 million housing starts each year with over 2 million between 2004 and 2007. After the crash, that number collapsed to half a million. It didn’t get up to over a million again until 2020 when developers were hit with Covid-19, the lockdowns and all the construction delays those things entailed.

It’s hard for there to be a crash when demand so drastically outstrips supply.

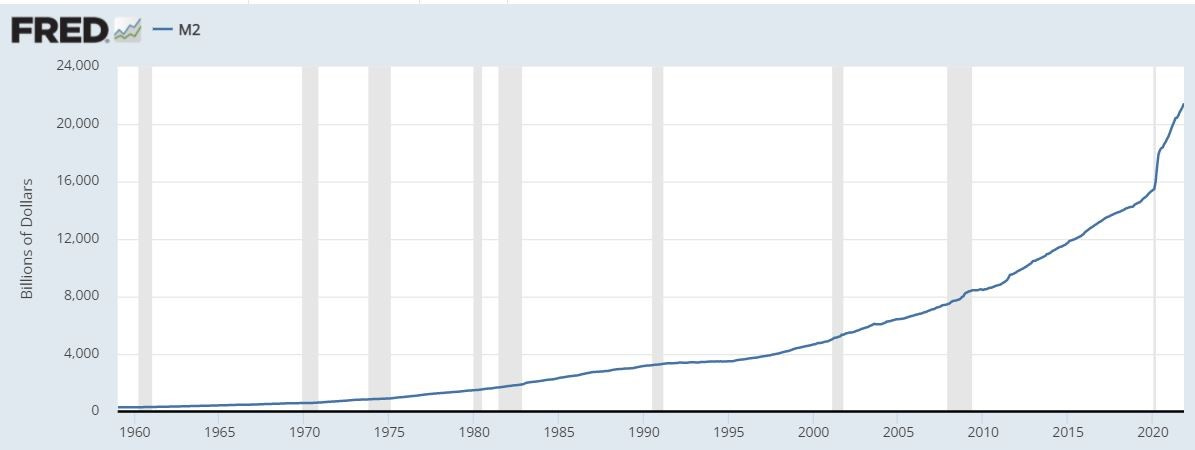

Finally, there’s the sheer volume of money the Fed has printed. Something like 40 percent of all the money in circulation was created in 2020. And 2021 wasn’t that much different.

Supply chain disruptions certainly haven’t helped, but I think it’s safe to say that inflation is here to stay.

Thus, real estate doesn’t even have to go up in value in real terms for its price to continue to appreciate nominally at a fairly fast pace. And of course, while the price may only be going up nominally, the mortgage won’t go up at all. In fact, it will go down as you pay off some of the principal each month.

Thus, in real terms, you’re getting wealthier even if real estate appreciates no faster than inflation… assuming of course, that you buy a property that cash flows and that you have long-term, fixed rate debt on the property.

Conclusion

The real estate market will likely slow down, if only for reasons of general affordability. And you should never buy without any margin whatsoever. But the time to get into real estate is now… at least it’s now if you can get long-term, fixed rate debt at the absurd terms they’re currently offering.

Trust me, those terms won’t last that much longer.